At RPR Legal Nexus in Kochi (Ernakulam), Kerala, we focus on consumer protection law, insurance disputes and grievance remedies, and medical negligence or hospital liability matters. We handle claim repudiation, claim delays, cashless denial disputes, unfair deductions, hospital billing issues, and patient rights concerns with a structured strategy based on evidence, timelines, and legal compliance. Our services include legal notices and reply notices, pre-litigation negotiation, mediation and out-of-court settlement support, and representation before the District, State, and National Consumer Commissions (DDRC, SCDRC, NCDRC).

Expertise, Integrity, Results – 5 Stars

★★★★★

RPR Legal Nexus

Safeguarding Your Rights and Interests

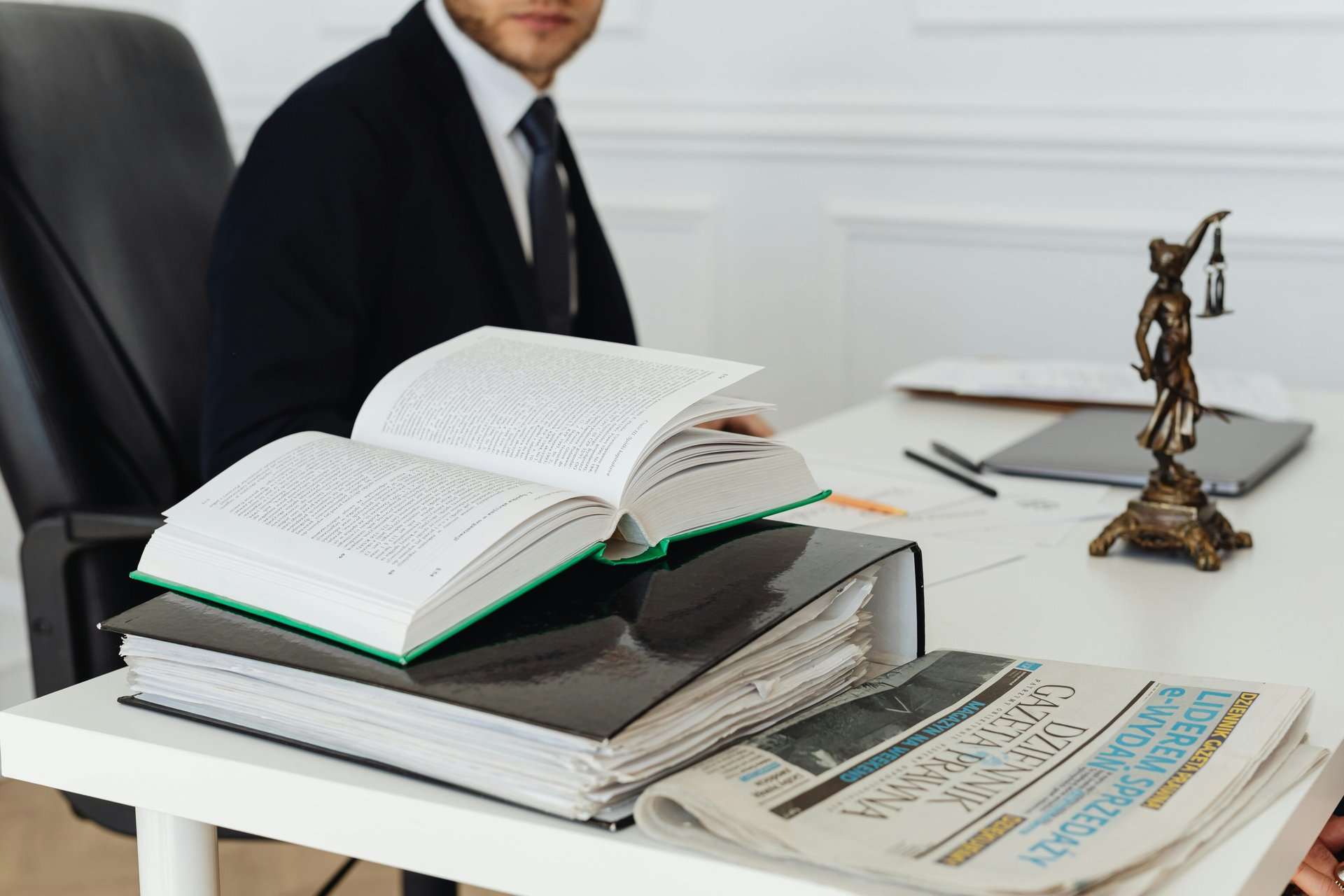

Navigating legal challenges can be overwhelming, but at RPR Legal Nexus, we simplify the process with strategic legal solutions that protect your rights and interests. Whether you are facing a legal dispute, seeking legal counsel, or require professional documentation, we are here to assist you every step of the way.

Civil Litigation

Representation in civil disputes, including contract disagreements, property matters, and other legal conflicts.

Consumer Protection

Resolving disputes related to defective products, misleading advertisements, fraudulent business practices, and e-commerce issues. We are dedicated to ensuring justice and fair treatment for our clients.

High Court Matters

Criminal Defense

Providing strong defense strategies for individuals facing criminal charges.

Handling cases and appeals in the High Court of Kerala with expertise and diligence.

Cyber Law

Addressing legal issues in the digital world, including data protection, cyber fraud, and online security concerns.

Legal Drafting

Preparing well-structured legal documents with precision and legal expertise.

Legal Advice

Offering strategic, informed counsel tailored to individuals and businesses.

offers specialized legal services to address bank account freezing issues and insurance disputes, providing swift and effective solutions to safeguard your financial interests.

Bank Account Freezing and Insurance-Related Disputes

Get in touch

We're here to help and answer any questions you may have. Contact us through . Don’t hesitate to ask we’re happy to assist you! 😊

Seasoned Legal Experts Your Dedicated Champions for Justice

Experienced Legal Professionals – Our team comprises highly skilled lawyers with extensive courtroom experience.

Client-Centric Approach – We prioritize your legal needs with tailored strategies.

Transparent Communication – We ensure clear, honest, and effective legal guidance.

Comprehensive Legal Support – A full spectrum of legal services under one roof.

Commitment to Justice – We advocate for fairness and protect our clients' rights.

Why Choose RPR Legal Nexus?

Your Legal Solution Starts Here

To uphold justice and fairness.

To empower individuals with legal knowledge.

To deliver innovative legal solutions in an evolving legal landscape.

To combat cyber fraud and online threats.

To provide unwavering legal representation and strategic advocacy.

By blending legal expertise with professionalism, we ensure that our clients receive dedicated legal support and practical solutions.

About us

RPR Legal Nexus is a trusted law firm specializing in Consumer Law, Cyber Law, Civil Litigation, Criminal Defense, High Court Matters, Legal Drafting, and Legal Advisory Services. With extensive experience across diverse legal domains, we offer strategic and effective legal solutions to safeguard the rights of both individuals and businesses. Our expertise also extends to Bank Account Freezing and Insurance-Related Disputes, ensuring comprehensive legal support for our clients.

150+

Happy clients

Connect

Support

Legal

+919400222945

RPR Legal Nexus© 2026. All rights reserved.

Connect with our expert legal team for personalized assistance and to schedule your free consultation. We're here to help you navigate your legal journey.